With home prices rising quickly, a lot of people are concerned that we are in a housing bubble and that the housing market will crash and there are going to be a lot of foreclosures flooding the market. I completely understand their concern, so let’s talk about this.

What is a housing bubble?

A housing bubble is a situation in which the market price of residential real estate sharply rises. The rising prices create the expectation of future price growth. That expectation attracts new buyers as well as speculators who invest in the market, hoping to profit.

It is very true that the market price of residential real estate has risen. And probably more than anyone expected, especially since what we went through in the spring of 2020.

However, this is the result of natural market forces. Low interest rates create demand. Factor in that people are spending more time at home and are realizing they need more space, they need a home office, they want a pool or they want to trade up. There are any number of reasons why there is high demand.

What Happens When a Housing Bubble Pops?

When a housing bubble pops, prices sharply fall, leaving many homeowners with negative equity (they owe more than their home is worth).

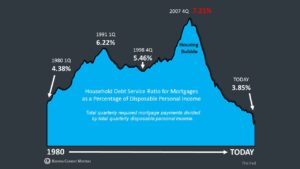

It is true that right now, according to the Fed,

“Mortgage balances—the largest component of household debt—surpassed $10 trillion in the fourth quarter, increasing by $182 billion to $10.04 trillion at the end of December.”

That is a whole lot of mortgage debt. So it would stand to reason that if prices fall, a lot of households would have negative equity. However, is that really the case?

Did you know that about 42% of the houses in the US have no mortgage at all? And unlike the last housing crises, the number of cash out refinancing that has occurred, even with these low interest rates, is quite low. The percentage of disposable income that people pay for housing is also much lower than it has been in the past.

Does that mean there are no households in trouble? Of course there are. There are millions of people in mortgage forbearance. Not all of them are in trouble, but I know some are. And if you are in trouble, I want you to know that you have options. You have to get ahead of this and not ignore your situation. If you need help, feel free to reach out to me and I can show you what your options are.

Normally, there are about 200,000 homes that go into foreclosure every quarter, for about 800,000 a year. With the moratorium, that has stopped. However, eventually these homes will hit the market. Most likely they will not all come at once, and there won’t be a so called flood.

Supply And Demand

And this also will not be a part of a so called housing bubble popping, because there is no housing bubble. Home values are rising as a part of natural market forces. Normal supply and demand does not constitute a housing bubble.

Even if interest rates rise and more homes enter the market place, we still have a long way to go before we have an over supply of houses and we no longer have a seller’s market. Without that, home prices will continue to rise.

So what do you think? Housing Bubble? Yea or nay? Share your thoughts in the comments.

Leave a Reply

You must be logged in to post a comment.